PV becomes increasingly attractive for the finance industry

Technical due diligence: Independent engineers scrutinize the technical plant design. © Andreas Schlegel

Until 2009, manufacturing and sales of technical components were the focus of solar business. For this reason, photovoltaic systems were valued first and foremost according to the system costs per kW of peak power. Now, however, photovoltaics is gaining an ever larger presence in the energy industry, and must therefore begin to gauge itself by the cost price per kilowatt hour. This not only includes the system costs, but also every bit of expenditure on realizing the solar project, the operating costs and financing.

In the past, the prime focus of photovoltaic business was on technical components. Today, trade centers increasingly on projects, financing and exploitation rights, which makes photovoltaics attractive for the finance industry. Financing models taken from classic manufacturing industries are directing a significant flow of money into the solar industry. These include trading in turnkey projects, project rights and other forms of participation in companies that operate solar power plants – right through to the purchase and sale of entire power plants.

Price cuts

In 2011, the average cost of a turnkey solar power plant in Germany was 2,200 euros for each newly installed kilowatt of rated power (net, excluding sales tax). During the course of 2011, prices then fell by around 30 percent In the case of large-scale installations with capacities of 1 MW and above, prices are cheaper, at between 1,300 and 1,500 euros per kilowatt.

Banks provide financing in various ways. They either grant project loans via their house bank, meaning that the full risk will be shown on that bank’s books, or they form syndicates to spread the risk exposure. Private capital is also being used more and more to fund solar projects. Club deals are common, where several banks pool a loan together as part of a skeleton agreement, with each of them on different terms. One of the banks coordinates the syndicate and acts as a contact with the client (borrower). However, with this model, the time between application and approval is longer meaning that investment costs are higher.

Thin-film plants are at the bottom end of the scale, while monocrystalline silicon parks with tracking systems sit toward the top. New module technologies (thin-film silicon, CIs or CIGs) are now also increasingly being classed as creditworthy, particularly if they are used in projects that mix them with proven technologies such as crystalline modules.

Financing stands or falls with the actual annual solar power yield fed into the grid. Banks expect a return on project investment of at least eight to nine percent. Private investors take between four and five percent if they conclude long-term deals where the degree of risk is low. The strong market for large-scale plants that prevailed at times in Spain (2008), Germany (2010 and 2011) and Italy (2011) created unrealistic expectations of the returns that solar power was able to yield. The eurozone crisis and the withdrawal of state subsidization are therefore forcing photovoltaics to take a more realistic view of things – and enabling it to exploit its long-term advantages more successfully. Ever more investors are recognizing the fact that the technology has matured and the risk of default is low. The investment, and thus the prices it can achieve on the power market, is not linked to the uncertainties of the oil market. And the sun supplies its energy for free, which gives photovoltaics a fundamental advantage.

The benefit gained from minimal financial risk should not be underestimated, especially with large solar farms. These can be installed in small, modular units and financed, refinanced and traded in stages. This valuable aspect of photovoltaics means that it could soon drive out solar thermal power generation. Photovoltaics is being used more and more to create new power plant capacity, particularly in sun-rich countries of more southerly climes, where the hunger for energy grows day by day and where technology capable of grid-connected and stand-alone power generation is sought.

Thanks to the expansion of production capacities for modules and inverters across the globe, there are practically no further bottlenecks that could limit the growth of photovoltaics as an industry, and solar parks in particular. From now on, area and capital will be the critical factors. One consequence of this is that many module manufacturers also operate as developers of large solar parks, as technology is usually bought directly from producers in this business segment.

Before we are able to assess the competitiveness of photovoltaic power compared to conventional energy sources, consideration must be given to the Levelized Cost of Energy (LCOE), which determines precisely what costs are incurred when generating solar power. The LCOE is0.5 stated in either euros or US dollars per kWh and takes into account the total cost of generating power, including investment costs for the plant itself, operating and maintenance costs, and other variable costs for the entire lifetime of the photovoltaic system.

According to the report titled “Solar Photovoltaics: Competing in the Energy Sector” published in September 2011 by EPIA, the cost of capital – expressed as the weighted average cost of capital (WACC) – is a key factor in the LCOE. The report states that the cost of capital has a greater impact on the LCOE than module prices, insolation at the site and plant lifetime. An academic paper on the importance of LCOE calculations for photovoltaic project developers and market stability was published in early 2011 in Energy and Environmental Science. The paper gives an insight into how photovoltaics would compete in the energy sector if LCOE calculations were applied to the cost side of the grid parity equation and then comparisons made between the actual electricity prices and those that are forecasted.

Loans are never granted without security. Examples of securities include the transfer of ownership of the PV plant, the transfer of rights from project contracts (delivery contracts, operating and maintenance contracts, contracts of use and occupation for the site, insurance20302027 contracts), encumbrances, pledging of the operator’s account or pledging of shares in the business. In the past, project financing was sometimes too tight, which led to non-performing loans. For this reason, banks often set requirements for the content of project contracts, or place stricter demands on the use of cash flow (reduced profit distribution). In addition, they require the quality of the installation to be inspected by external experts (technical due diligence). It is not uncommon for two independent yield reports to be requested.

A due diligence assessment serves to analyze the strengths and weaknesses of a project, as well as to evaluate its risks and estimate its economic value. The analysis particularly focuses on technical and material defects, legal and financial risks, and circumstances that stand in the way of a project being realized or being profitable. If risks are detected, this could lead to contractual allowances being made in the form of price reductions or guarantees – or in extreme cases, could trigger the abandonment of negotiations.

RES-LEGAL

The free RES-LEGAL database provides an overview of the manifold subsidization models in Europe and well as the stipulations and guidelines on grid connection. It contains all important legal regulations on subsidies and the feed-in of power from renewable sources within the EU. The collection of models for remuneration, tax incentives and certificates as well as grid access comprises 27 countries. A search assistant enables users to analyze and compare legislation in the different countries.

www.res-legal.eu

Legal due diligence

This step examines the legal basis of a project from purchase or rental of property to feeding in. Checks are made on the application to the utility as well as on the operating, maintenance and insurance contracts. Experienced project developers use standardized templates to exclude major risks.

Tax due diligence

Experts check the tax aspects of a project, such as corporation income tax, trade tax and income tax, value added tax, tax on profits, real property tax and land transfer tax, as well as taxes incurred during operation. Such an analysis includes tax incentives and depreciations.

Technical due diligence

Independent engineers scrutinize the technical plant design. This includes: system planning (yield forecast, plant layout, inclination and alignment of modules, ground survey, distance from feed-in point, number of feed-in points, grid capacity), specification and selection of components, tenders and order placement, installation, technical quality management and building quality management, operational monitoring and safety, manufacturers’ and installers’ guarantees and warranties, creditworthiness of suppliers, theft and vandalism protection (fencing, CCTV), and the costs of maintenance and land management (for example mowing and pruning).

Financial due diligence

The last phase before a loan is granted concerns financial aspects: required investments (capex), costs for the property and yields from any future sale, expected solar yield, costs for operation and maintenance (opex), liquidity reserves, insurance, costs for dismantling and recycling the plant after the end of its service life. The cash flow, taxes and debt services are used as a basis for evaluating profitability, which is the deciding factor in granting loans.

To date, solar power plant project developers have commonly also assumed responsibility for maintaining and operating plants on behalf of investors. However, for the duration of the warranty period, a conflict of interests arises that is typically settled at a disadvantage to the investor. As a result, the fields of planning and operating large-scale power plants are increasingly going their separate ways, not least because ever more attention is being paid to expenditure on operation and maintenance (O&M) in a bid to limit the overall costs of investment.

The specific yield of an investment can easily be quantified using an empirical formula that illustrates the key operating parameters of the installation. This formula was devised by analysts at Solarpraxis AG in order to optimize plant configuration and the use of financial resources. If the specific yield of the plant is then multiplied by the availability of the inverter to the grid, this gives the total yield taking into account every euro spent.

In Germany, many other EU countries, and in several others besides, solar electricity is sold to grid operators at a statutorily guaranteed feed-in tariff. During the first half of 2012, these feed-in tariffs were dramatically reduced, and in some cases stopped altogether, particularly for large-scale power plants.

The market for large solar power stations is therefore likely to mature within a short space of time. The era of statutorily guaranteed feed-in tariffs will soon be dead, and the dawn will rise on that of directly marketed photovoltaic power. The solar industry has reached this stage within just a few years. Throughout 2012 and 2013, solar power plants are likely to be subject to compensatory pricing before they finally become governed by the free interplay of market forces in the energy sector.

In many countries, expansion quotas are capping growth. Examples of this can be seen in Spain and Italy, where total spending on feed-in remuneration is limited to six million euros per year. In a different model, the German government is making all further development of feed-in tariffs dependent on an annual expansion corridor of between 2.5 and 3.5 GW. If feed-in tariffs were to disappear completely in the near future, however, the state would have virtually no grounds for capping photovoltaic expansion.

The picture outside of the EU is also heterogeneous. India is considering a feed-in law with guaranteed remuneration. The picture outside of the EU is also quite diverse. India is considering a feed-in law with guaranteed remuneration. China intends to designate large areas for solar power plants with capacities of several GW, though so far has only introduced uniform feed-in tariffs for small-scale installations. There, projects are controlled exclusively by the state and put out to tender through auctions.

Tax incentives play an important role in the USA (Investment Tax Credits: ITC), and can reach up to 30 percent. These sums can be directly offset against tax liabilities, and if no tax is due, the ITCs are paid out to investors as negative tax. In addition, some states pay out for every kWh fed into the grid, while others offer tax bonuses and subsidies. Power Purchase Agreements (PPA) are the preferred business model for large-scale solar power plants. As part of these agreements, the solar power is sold to one energy utility or one large customer for ten or 15 years. The project tenders commonly invited at auctions in many Asian, Arab and some European countries basically work on a similar financing model, only the price is decided during the auction. It is not uncommon for lengthy negotiations to ensue afterwards due to investments being only barely covered. Little is likely to change in this practice in China, as the country has no private energy utilities. In countries such as India and Thailand, however, an economic mindset will increasingly win through and spur the markets on.

New feed-in tariff in Germany

The savage cuts to feed-in tariffs did nothing to dampen the photovoltaics boom in Germany during 2011. In March 2012, the German parliament voted in favor of drastically lowering the tariffs again from April 1, 2012. Now only three power classes remain: small rooftop systems with outputs up to 10 kW (19.5 euro cents per kWh), larger roof-mounted installations with outputs between 10 kW and 1 MW (16.5 euro cents) and plants with outputs of 1 to 10 MW installed on roofs or on the ground (13.5 euro cents). Starting in May, remuneration for solar power fed into the grid will be reduced by one percent every month. Operators of small installations will be required to consume 20 percent of the power they generate on site or to sell it independently. A figure of ten percent is required from medium-sized plants with an output of up to 1 MW. Although power from larger MW-scale installations is remunerated in full, very large plants with outputs over 10 MW no longer receive any remuneration whatsoever. Transitional provisions are in place for rooftop and ground-mounted plants that apply until the end of June 2012, and for redeveloped brownfield sites until late September 2012.

Furthermore, in future the outputs of all MW-scale plants within a four-kilometer radius of one another will be added together. If they are found to have a cumulative capacity of over 10 GW, these sub-generators will no longer receive remuneration, even if they belong to different owners. This rule will apply for an interim period of two years. And even the concept of commissioning a solar installation has been reformulated. In future, it will no longer be possible to put solar arrays into operation that do not have inverters. However, the connection to the grid will continue to have no impact on the feed-in tariff it receives.

(As the legislative process is in the course of being completed in 2012, these regulations may be subject to change.)

The Lüptitz citizens’ solar power plant (Germany) is run by a cooperative of private persons. © Solverde Bürgerkraftwerke Gesellschaft/Norbert Meise

Banks require the quality of the installation to be inspected by external experts. © Tom Baerwald

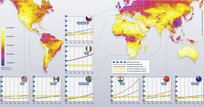

Annual global irradiation and solar electricity potential

The Helbra solar farm (Saxony-Anhalt, Germany) has a total output capacity of 11.7 MW. © Parabel AG

The PV plant is situated on a 18,000 m2 property on the outskirts of the German town of Adorf and generates 1.2m kWh of electricity per year. © BLG Projekt GmbH

The PV sound barrier is located on a motorway in Germany, close to Munich’s airport, with a length of 1.2 km and a capacity of 500 kWp. © Isofoton

The Reckahn Solar Park has a capacity of 37.7 MWp and is located in Reckahn, Southwest of Berlin, Germany. © Belectric Solarkraftwerke GmbH